Leapmotor International sets the precedent for Chinese car production in Europe: an automotive industry analysis

The Brussels Motor Show 2025 highlighted the evolving dynamics of the European automotive market, as Chinese automakers take strides toward establishing themselves as key players in the region. This year, Leapmotor stood out, strategically positioned between the displays of mass-market brands Fiat and Opel belonging to its new joint venture (JV) partner, Stellantis.

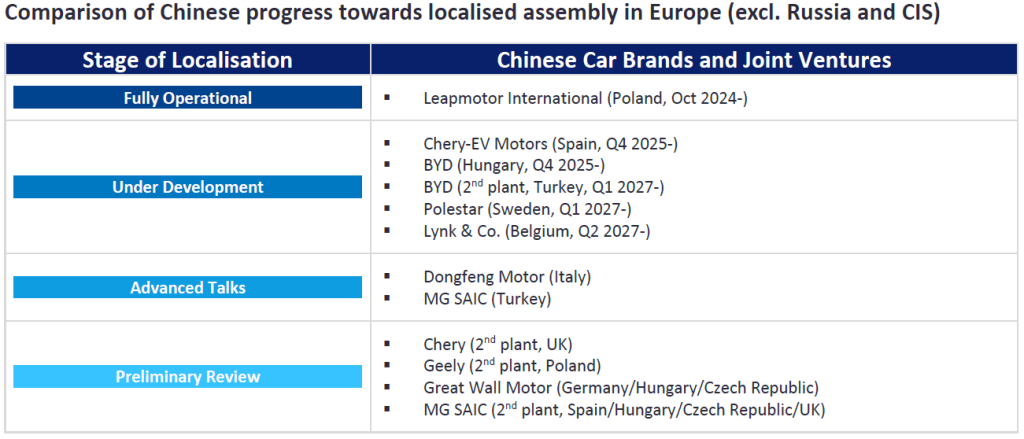

Having finalised their partnership in May 2024, giving birth to Leapmotor International, the company began selling imported Leapmotor C10 and T03 models in 13 European countries from late September 2024. The following month, it commenced full-scale assembly at Stellantis’ Tychy plant in Poland, uniquely becoming the first Chinese carmaker to accomplish this in the EU.

Leapmotor’s physical presence at the show not only symbolises its ongoing integration into the Stellantis product mix, but also the broader incorporation of low-cost Chinese Electric Vehicles (EVs) into the European market.

A Strategic Collaboration

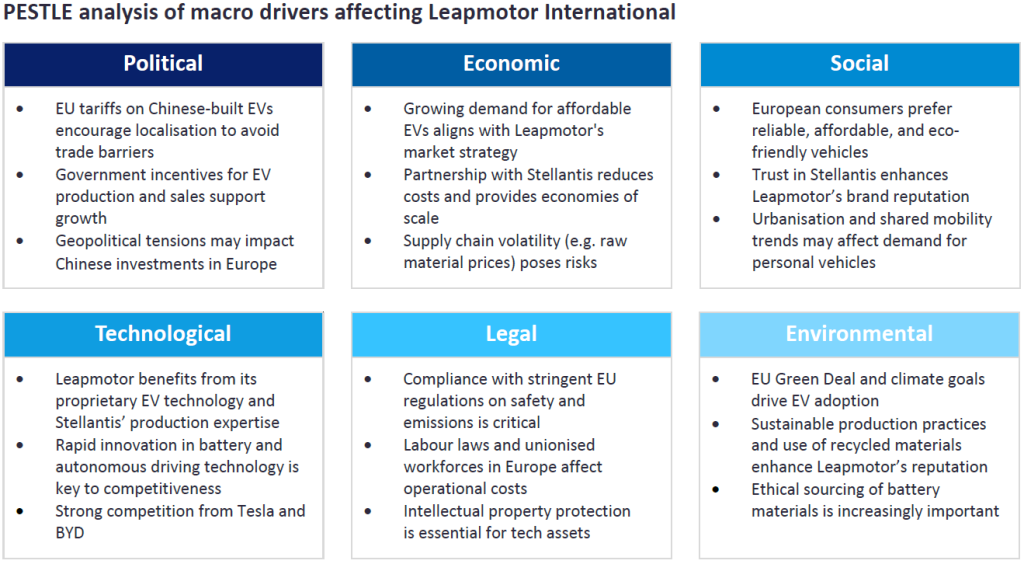

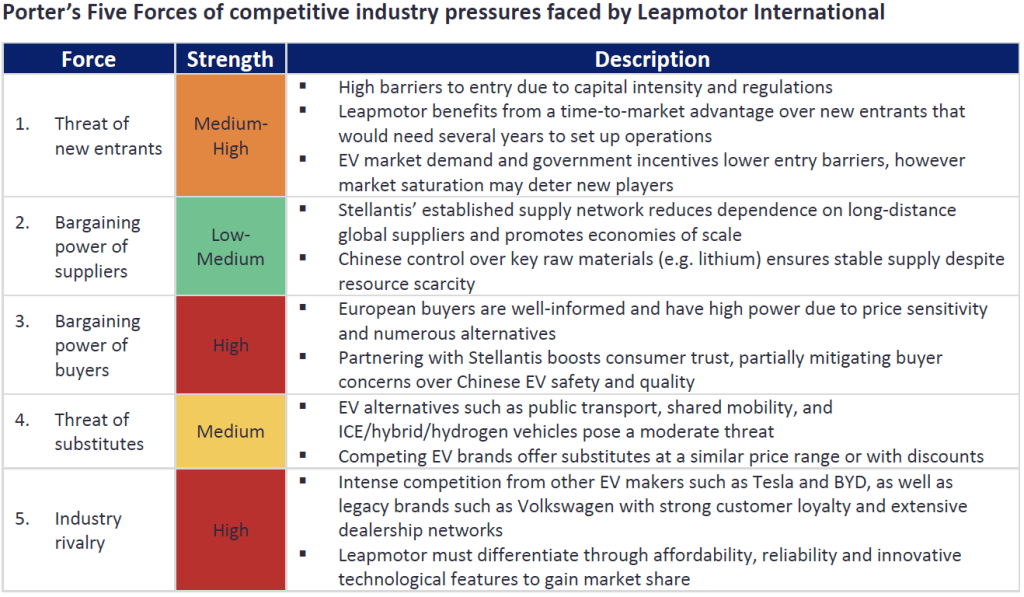

Leapmotor International represents a step-up in Chinese automakers’ efforts to gain a foothold on the European continent. Created to undercut existing electric models on the European market, the tie-up aims to emulate the success of established and mass-produced Stellantis marques, offering affordable yet technologically advanced vehicles tailored to European consumer preferences. This arrangement leverages Stellantis’ extensive infrastructure and supply base, helping to offset some of its excess capacity in the region, while concurrently mitigating the effect of the EU’s newly imposed tariffs on Chinese-built EVs.

Financially, Stellantis benefits from greater exposure to the affordable EV segment, while Leapmotor gains from more secure access to the lucrative European market amid slowing domestic conditions in China. On the other hand, the recent trade dispute between China and EU highlights the inherent geopolitical risk involved in such an enterprise, with plans for further investment in Poland now being actively discouraged by the CCP. Reportedly, Leapmotor is considering adding new models to a different Stellantis facility in either Germany or Slovakia, as both of these countries opposed the anti-Chinese EV tariffs, though this may simply be a ploy to gain leverage in the current negotiations.

Access the most comprehensive Company Profiles

on the market, powered by GlobalData. Save hours of research. Gain competitive edge.

Company Profile – free

sample

Your download email will arrive shortly

We are confident about the

unique

quality of our Company Profiles. However, we want you to make the most

beneficial

decision for your business, so we offer a free sample that you can download by

submitting the below form

By GlobalData

Competing Chinese Car Production in Europe

Chery Group will likely be the next Chinese car company to localise production in Europe, expected around Q4 2025 when it plans to begin assembling Chery and Omoda models at the former Nissan factory in Barcelona.

This was made possible through a JV with Spanish manufacturer EV Motors that was then used to acquire the plant, providing another example of how entering into a partnership over an existing facility can reduce the lead time for Chinese automakers, accelerating their market entry compared to other brands that are building their own factories from scratch.

BYD, for instance, is scheduled to open its Szeged car plant in Hungary around Q4 2025 as well, however it first announced its plans back in December 2023, several months before the Chery-EV Motor JV was signed in April 2024. Moreover, the next confirmed Chinese facility – a BYD plant in Turkey – will not be operational until Q1 2027, while Geely’s Polestar and Lynk & Co brands are not slated to join the group’s Volvo Car factories in Sweden and Belgium until later that year.

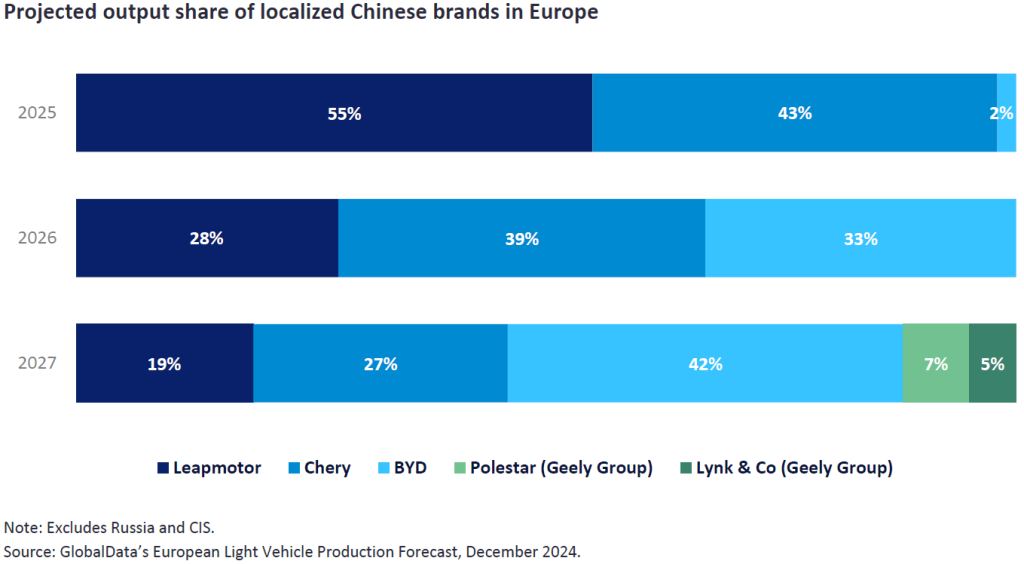

Despite their quicker time-to-market, we can expect the localised production share of the Chinese JVs to diminish over time, as the brands with larger, purpose-built car factories begin ramping up assembly. Notably, Leapmotor International and Chery-EV Motors are projected to dominate this year with a combined 98% of Chinese car output in Europe, falling to roughly two-thirds in 2026, and then less than 50% in 2027 due to the expansion of BYD and Geely Group manufacturing activity.

Several more Chinese brands have long-term aspirations in Europe, though the manner of their arrival (JV with access to a shared facility, outright purchase of an underutilised factory, or construction of their own plant from scratch) will certainly affect the speed and scale of their market entry. This trend mirrors the transformation of the Russian automotive sector following the start of the Ukraine War, with Chinese manufacturers filling the void left by departing Western firms, predominantly through contract assembly with local Russian manufacturers instead of partnerships or more direct forms of investment. Indeed, there is only a single Chinese-owned plant in Russia, constructed by Great Wall Motor in 2019 before the global pandemic, and little appetite for further localisation beyond simply importing more prefabricated Chinese kits for final assembly.

Summary

The Brussels Motor Show 2025 displayed the progress of Chinese carmakers towards their ambitious goals of European expansion, with Leapmotor presented as the first of a new wave of Chinese brands localising production on the continent. In the near to medium term, the success of JVs like Leapmotor International will depend on their ability to overcome initial skepticism over quality, and adapt to local market conditions on a competitive, regulatory and geopolitical level as trade disputes mount around the world. In the long term, growth will rely on brand building, localised R&D, and investment in more efficient production processes. Chinese automakers are well-positioned to capture a growing share of the market, and as they continue to expand their European footprint, their influence on the region’s automotive industry is only set to increase for years to come.

Jeremy Worlock, Analyst, Production Forecasts, GlobalData

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.

link

Stocks to Buy in 2026")