Business Loan Requirements: What You Need to Qualify

⏰ Estimated read time: 8 minutes

Here are seven things lenders generally look at to decide whether you qualify for a loan.

We’ll start with a brief questionnaire to better understand the unique needs of your business.

Once we uncover your personalized matches, our team will consult you on the process moving forward.

1. Personal and business credit scores

Personal credit scores indicate your ability to repay personal debts, such as credit cards, car loans and mortgages. Small-business lenders require a personal credit check because they want to see how you manage debt.

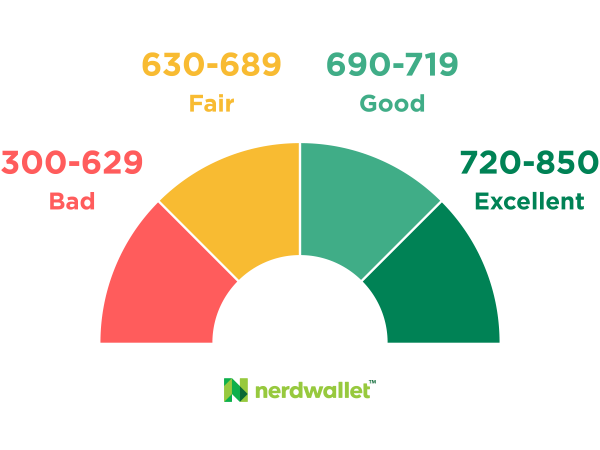

NerdWallet’s credit score bands, used for general guidance

Fast ways to build your personal credit include disputing any inaccuracies in your report and paying bills on time and in full.

2. Annual revenue

Many lenders will only consider businesses that bring in at least a minimum monthly or annual revenue. Lenders look at your revenue to make sure that you have enough cash flow to afford your loan.

How much cash flow you’ll need depends on the individual lender — for example, online lender OnDeck requires $100,000 in annual revenue to qualify for its line of credit, while Bank of America’s minimum is $250,000 for its secured business loans.

Debt service coverage ratio

A similar financial metric your lender may consider is your debt service coverage ratio (also known as DSCR). This ratio compares your available operating income to your current debt obligations. To calculate your DSCR, you divide your annual operating income by your total annual debt payments.

For example, if your annual income is $150,000 and your total debt payments are $100,000, your debt service coverage ratio would be 1.5. Generally, lenders want to see a ratio higher than 1, typically a minimum of 1.25, as this indicates that your cash flow is sufficient to cover your debt obligations.

3. Years in business

Lenders use your time in business as a quick measure of success. The longer you’ve been operating, the more likely you are to have money to repay your debts.

4. Business industry and size

Every industry has a different risk level — and some industries, like restaurants and beauty services, can be considered high risk because they’re more likely to have inconsistent revenue.

There are also certain industries that many lenders don’t work with at all. These typically include adult entertainment, drug dispensaries or products, gambling and money service businesses.

-

You must be a for-profit company.

-

You can’t operate in an ineligible industry, like real estate investing, gambling or political lobbying activities.

-

You must be current on all government loans with no past defaults — you’ll be disqualified if you’ve been late (you haven’t paid within 90 days of the due date) on a federal student loan or government-backed mortgage, for instance.

5. Business plan and loan proposal

These documents should clearly demonstrate that you will have enough cash flow to cover ongoing business expenses and the new loan payments. This can give the lender more confidence in your business, increasing your chances at loan approval. On the other hand, if you’re a new business that doesn’t have existing revenue to show a lender, a thorough business plan can help convince it that you will be successful in the future.

Use NerdWallet’s business loan calculator to estimate your monthly loan payments:

Calculate estimated payments, then see if you qualify for a business loan

Over the course of the loan, expect to pay

$0.00/mo

Payment breakdown

$0.00

Get personalized small-business loan rates to compare

with Fundera by NerdWallet

6. Collateral or personal guarantee

Each lender has its own rules, so ask questions if you’re unsure what’s required.

7. Business and financial documentation

-

Personal and business income tax returns.

-

Financial documents, such as profit and loss statements, balance sheets and cash flow statements.

-

Personal and business bank statements.

-

A photo of your driver’s license.

-

Commercial leases.

-

Business licenses.

-

Articles of incorporation.

-

Proof of collateral.

-

Business plan.

-

Legal contracts and agreements.

-

A resume that shows relevant management or business experience.

-

Financial projections if you have a limited operating history.

Online lenders may provide a streamlined application process with fewer documents and faster underwriting.

🤓 Nerdy Tip

When completing your business loan application, it’s important to double check that your documentation is accurate and up to date. Not only will this speed up the funding process, but it can also help prevent automatic rejections. If a lender is using automated underwriting and you input incorrect information, it can result in an automatic rejection — even if you’re qualified.

Find the right business loan

Frequently Asked Questions

Although business loan requirements vary from lender to lender, you’ll generally need good credit, strong finances and an established business history to qualify for a loan. Traditional lenders typically have the strictest requirements, whereas online lenders are more flexible.

Banks generally require that you have good to excellent credit (score of 690 or higher), strong finances and at least two years in business to qualify for a loan. They’ll likely require collateral and a personal guarantee as well.

You’ll typically need to provide detailed paperwork as part of your application — and some banks will require you to apply in person.

Each lender will have unique documentation requirements, but at the very least, you’ll likely need to provide:

-

Business and personal bank statements.

-

Business and personal tax returns.

-

Financial statements, like balance sheets and income statements.

Traditional lenders typically require more paperwork than online lenders.

Former NerdWallet writer Steve Nicastro contributed to this article.

link